Statistical Methods

Statistical methods are used to compare the difference between distributions. In some cases, a divergence is used, which is a type of distance metric between distributions. In other cases, a test is run to receive a score.

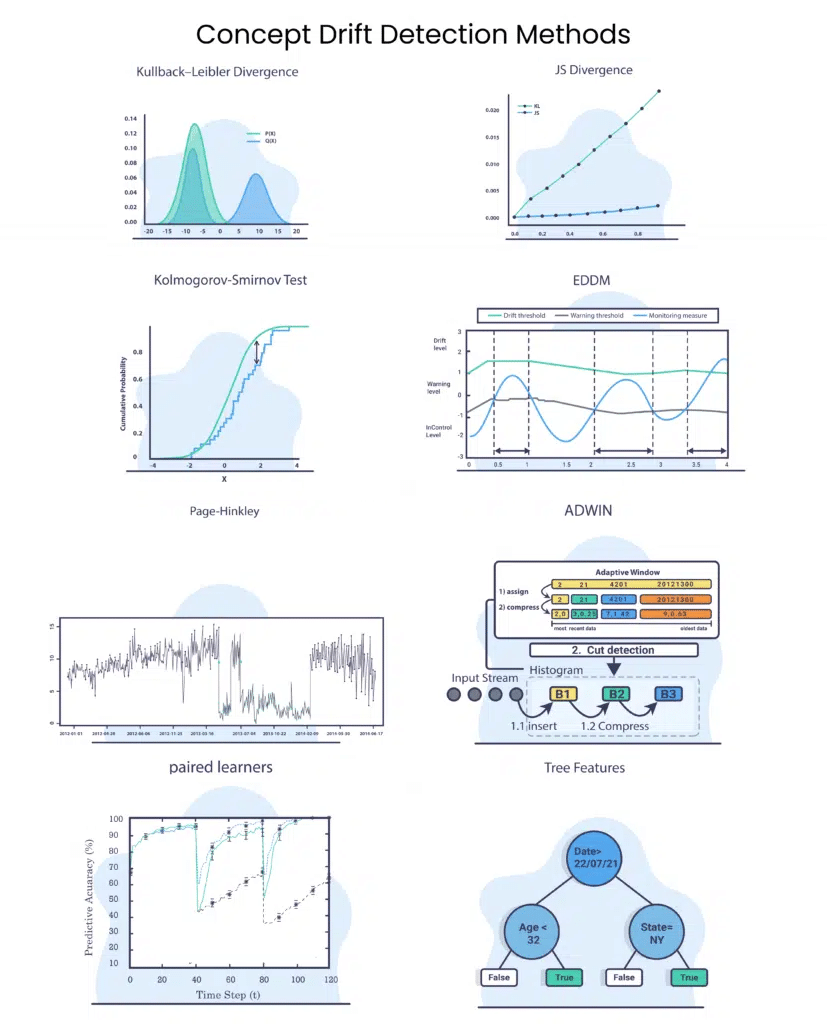

Kullback–Leibler Divergence

Kullback–Leibler divergence is sometimes referred to as relative entropy. The KL divergence tries to quantify how much one probability distribution differs from another, so if we have the distributions Q and P where the Q distribution is the distribution of the old data and P is that of the new data we would like to calculate:

* The “||” represents the divergence.

We can see that if P(x) is high and Q(x) is low, the divergence will be high.

If P(x) is low and Q(x) is high, the divergence will be high as well but not as much.

If P(x) and Q(x) are similar, then the divergence will be lower.

Where  the mean between P and Q

the mean between P and Q

Kolmogorov-Smirnov Test

The two-sample KS test is a useful and general nonparametric method for comparing two samples. In the KS test we calculate:

Where  is the empirical distribution function of the previous data with

is the empirical distribution function of the previous data with  samples and

samples and  is the empirical distribution function of the new data with

is the empirical distribution function of the new data with  samples and

samples and ![F_{n}(x) = \frac{1}{n} \displaystyle\sum_{i=1}^n I_{[- \infty,x]}(X_{i})](https://www.aporia.com/wp-content/ql-cache/quicklatex.com-7436b76d84f13ea7c30ebb0d66a68c81_l3.png "Rendered by QuickLaTeX.com") . The

. The  is the subset of samples x that maximizes

is the subset of samples x that maximizes  .

.

The KS test is sensitive to differences in both location and shape of the empirical cumulative distribution functions of the two samples. It is well suited for numerical data.

Statistical Process Control

The idea of statistical process control is to verify that our model’s error is in control. This is especially important when running in production as the performance changes over time. Thus, we would like to have a system that would send an alert if the model passes some error rate. Note that some models have a “traffic light” system where they also have warning alerts.

Drift Detection Method/Early Drift Detection Method (DDM/EDDM)

The idea is to model the error as a binomial variable. That means that we can calculate our expected value of the errors. As we are working with a binomial distribution we can mark =npt and therefore  .

.

DDM

Here we can raise:

- A warning when

- An alarm when

Pros: DDM shows good performance when detecting gradual changes (if they are not very slow) and abrupt changes (incremental and sudden drifts).

Cons: DDM has difficulties detecting drift when the change is slowly gradual. It is possible that many samples are stored for a long time, before the drift level is activated and there is the risk of overflowing the sample storage.

EDDM

Here by measuring the distance of 2 consecutive errors, we can raise:

- A warning when

- An alarm when

, where

, where  is usually 0.9

is usually 0.9

The EDDM method is a modified version of DDM where the focus is on identifying gradual drift.

")

CUMSUM and Page-Hinckley (PH)

CUSUM and its variant Page-Hinckley (PH) are among the pioneer methods in the community. The idea of this method is to provide a sequential analysis technique typically used for monitoring change detection in the average of a Gaussian signal.

CUSUM and Page-Hinckley (PH) detect concept drift by calculating the difference of observed values from the mean and set an alarm for a drift when this value is larger than a user-defined threshold. These algorithms are sensitive to the parameter values, resulting in a tradeoff between false alarms and detecting true drifts.

As CUMSUM and Page-Hinckley (PH) are used to treating data streams, each event is used to calculate the next result:

CUMSUM:

where g represents the event, or for drifting purposes, the input/output of the model- When

an alarm is raised, and set

an alarm is raised, and set

are tunable parameters

are tunable parameters- Note that CUMSUM is memoryless, one-sided or asymmetrical so it can detect only an increase in the value.

Page-Hinckley (PH):

When  an alarm is raised, and set

an alarm is raised, and set

Time Window Distribution

The Time Window Distribution model focuses on the timestamp and the occurrence of the events.

ADWIN

The idea of ADWIN is to start from time window  and dynamically grow the window when there is no apparent change in the context, and shrink it when a change is detected. The algorithm tries to find two subwindows of

and dynamically grow the window when there is no apparent change in the context, and shrink it when a change is detected. The algorithm tries to find two subwindows of  and

and  that exhibit distinct averages. This means that the older portion of the window –

that exhibit distinct averages. This means that the older portion of the window –  is based on a data distribution different than the actual one, and is therefore dropped.

is based on a data distribution different than the actual one, and is therefore dropped.

Recent Comments